Insurance Requirements for Apartment Renovations

Insurance requirements in Manhattan co-ops and condominiums are shaped by how New York buildings are constructed and governed. Apartments are privately owned or leased, but the systems that make them function are shared. Plumbing risers serve multiple units. Electrical infrastructure runs vertically through the building. Structural slabs extend beyond the footprint of a single residence. Ventilation, fire protection, and mechanical systems are interconnected.

Because of this integration, renovation risk is rarely isolated.

A plumbing error in one apartment can damage ceilings and flooring below within minutes. A demolition crew that removes material too aggressively can compromise adjacent finishes or disturb structural elements. Improperly protected electrical work can create fire hazards that extend beyond the renovation footprint. Even a small oversight can quickly become a multi-unit insurance claim.

Boards and managing agents evaluate renovation proposals with this reality in mind. Their concern is not whether a contractor is careful. Their concern is whether, if something does happen, the financial responsibility is clearly assigned and adequately insured.

That is the function of renovation insurance in Manhattan. It ensures that risk follows control.

How Contractor Insurance Allocates Risk

Contractor insurance is designed to respond to third-party claims arising from construction activity. In the context of Manhattan apartment renovations, that typically means bodily injury, property damage, or certain professional errors connected to the work.

If a worker is injured on site, if a neighbor claims water damage, or if a shared building component is affected, the contractor’s insurance should respond first. This protects the apartment owner and prevents the building’s master policy from absorbing avoidable losses.

Without adequate insurance, exposure shifts. An injured worker may pursue claims beyond statutory benefits. A neighboring unit owner may file suit against the building. The building’s insurer may pay a claim and then pursue recovery from the apartment owner. These secondary disputes are exactly what boards seek to prevent through strict insurance requirements.

Insurance documentation, when structured correctly, is not symbolic. It is a risk transfer mechanism embedded in the renovation approval process.

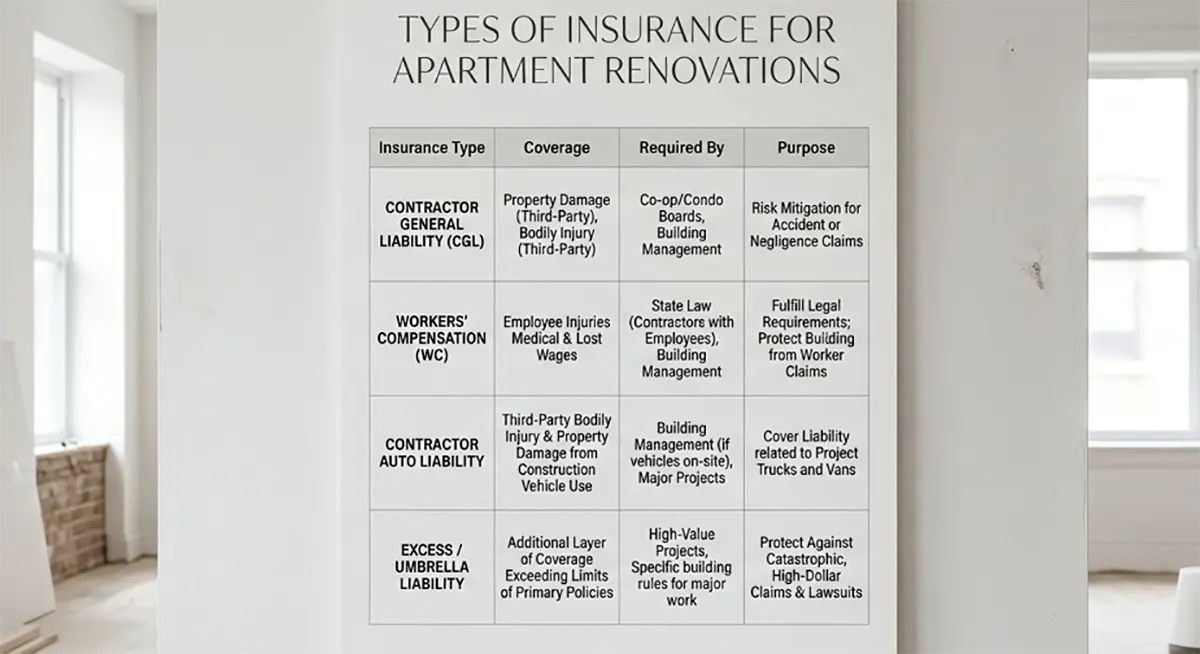

Core Insurance Policies Required for Manhattan Renovations

While each building sets its own standards, most Manhattan apartment renovation insurance packages include several consistent components.

Commercial General Liability Insurance

Commercial General Liability, or CGL, is the foundation of any construction insurance program. It provides coverage for third-party bodily injury and property damage arising from the contractor’s operations.

In Manhattan residential buildings, minimum limits are commonly one million dollars per occurrence and two million dollars aggregate. In higher-end properties or projects involving structural changes, boards often require higher limits or an accompanying umbrella policy.

CGL coverage funds legal defense and settlement costs if claims are brought by neighbors, visitors, building staff, or other affected parties. However, the existence of a CGL policy alone is not sufficient. The policy must be properly endorsed to extend protection to the building and managing agent.

Workers’ Compensation and Employer’s Liability

New York law requires employers to carry Workers’ Compensation insurance. This coverage provides medical benefits and wage replacement for employees injured on the job.

In Manhattan apartment renovations, workers’ compensation compliance is critical. If a contractor lacks proper coverage and a worker is injured, the unit owner and potentially the building may be drawn into litigation under New York Labor Law. Boards therefore review workers’ compensation certificates carefully before granting approval.

Employer’s Liability coverage complements workers’ compensation by addressing certain claims that fall outside statutory benefits.

Umbrella or Excess Liability Coverage

Umbrella or excess liability policies provide additional limits above the primary CGL policy. Many Manhattan buildings require umbrella limits between two and five million dollars, depending on project scope.

The rationale is straightforward. In a multi-unit environment, property damage claims can escalate quickly. If water affects several apartments, primary limits may be exhausted rapidly. Excess coverage ensures that adequate protection remains available.

| Coverage Type | What It Covers | Typical Limits | Notes |

|---|---|---|---|

| (R1) CONTRACTOR’S GENERAL LIABILITY (CGL) | 3rd-Party Bodily Injury & Property Damage | $1M Per Occur. / $2M Aggreg. | REQUIRED BY MOST NYC BUILDINGS, CO-OPS, & CONDOS |

| (R2) EXCESS / UMBRELLA LIABILITY | Extra Layer of CGL Coverage | $5M to $50M+ | FOR HIGH-VALUE, COMPLEX, OR HIGH-RISE PROJECTS. CHECK BUILDING RULES. |

| (R3) WORKERS’ COMPENSATION | On-Site Employee Injury Medical & Wages | State Mandatory | MUST VERIFY ALL SUBCONTRACTORS ARE COVERED |

| (R4) OWNER’S RENO ENDORSEMENT | Damage to Personal Property, Finished Work, Fixtures | Project Budget | CRUCIAL: UPDATE OWNER’S POLICY BEFORE START. OFTEN ADDED BY ENDORSEMENT. |

Professional Liability Insurance

If architects, engineers, or design-build contractors are providing professional services, professional liability insurance is required. Commercial General Liability policies exclude coverage for design errors. Professional liability fills that gap.

Projects involving load-bearing wall modifications, structural reconfiguration, or significant MEP redesign typically require proof of active professional liability coverage before boards approve plans.

Builder’s Risk Insurance

For full gut renovations or projects involving substantial material staging, builder’s risk insurance may be required. This policy covers materials and work in progress against events such as fire, theft, or vandalism.

Builder’s risk becomes particularly relevant when construction extends over a long period or when high-value finishes are stored on site prior to installation.

Understanding the Certificate of Insurance in Manhattan Renovations

The Certificate of Insurance, commonly referred to as a COI, is the document most frequently submitted to boards and managing agents. However, it is often misunderstood by apartment owners.

A COI is not the insurance policy itself. It is a summary issued by an insurance broker that lists coverage types, policy numbers, limits, and effective dates. It may also identify additional insured entities and describe the renovation location.

What the COI does not do is create coverage. The enforceable rights are contained in the underlying policy and its endorsements.

This distinction matters. A building may be listed as an additional insured on a certificate, but unless the proper endorsement is attached to the policy, the protection may not exist in practice. Managing agents who review insurance submissions carefully will request copies of endorsements, not just certificates.

For apartment owners, understanding this difference prevents frustration during the approval process. If a managing agent rejects a submission, it is often because required endorsements are missing or incorrectly structured.

Why Endorsements Matter in Manhattan Renovation Insurance

In most Manhattan apartment renovations, three endorsements are consistently required.

| Endorsement | What It Does |

|---|---|

| Additional Insured | Extends coverage under the contractor’s policy to the building entity and managing agent, allowing them to access defense and indemnification directly if a claim arises |

| Primary and Non-Contributory | Ensures the contractor’s insurance responds before the building’s master policy, preventing the building’s insurer from contributing to a claim that should be covered by the contractor |

| Waiver of Subrogation | Prevents the contractor’s insurer from seeking reimbursement from the building or unit owner after paying a claim |

These endorsements are not technical preferences. They are central to how risk transfer functions in a Manhattan renovation. Without them, coverage may exist on paper but fail in practice when disputes arise.

DIY or Hire a Pro? A Guide to Making Smart Renovation Decisions

The appeal of DIY renovation is real. There’s something genuinely satisfying about improving y

Timeline of a Manhattan Renovation: From Offer Letter to Move-In

You just signed the offer letter. Champagne is popped. You are already mentally placing the sofa in

What Happens If Your Contractor Pulls the Wrong Permit

Permit errors are more common on Manhattan renovation projects than most owners realize, and the con